In a context where environmental, social, and governance (ESG) issues are redefining the rules of the economic game, non-listed SMEs can no longer remain on the sidelines. They are increasingly called upon by their clients, financiers, and partners to demonstrate their commitment to sustainability.

Developed by the European Financial Reporting Advisory Group (EFRAG), the Voluntary Sustainability Reporting Standard for non-listed SMEs (VSME) is establishing itself as a simple, accessible, and strategic framework. Designed for small structures, this voluntary standard offers much more than a reporting framework :

- It paves the way for the seamless integration of responsible companies into the value chains of major economic players committed to a sustainable transition.

- It allows companies to achieve concrete recognition for their CSR approach.

A concrete response to the challenges of small businesses

SMEs committed to the sustainable transition often struggle to have their efforts recognized due to a lack of suitable tools. It is to fill this gap that EFRAG designed the VSME : a voluntary, proportionate, and structuring framework. It provides small structures with a clear and harmonized language to present their ESG actions in a credible, understandable, and valuable way. By facilitating extra-financial communication, the VSME strengthens the legitimacy of companies with their stakeholders, who are increasingly attentive to sustainable practices and the strategic role of companies in the transition toward a responsible economic model.

Thanks to its alignment with the principles of the CSRD, this simplified standard constitutes a real launchpad toward professionalized ESG reporting, without the administrative burdens of major standards. It allows SME managers to integrate sustainability into their strategy in a progressive manner adapted to their reality on the ground.

A modular structure designed for SME agility

The VSME standard is based on an architecture of two complementary modules : the basic module and the narrative module, allowing for a progressive entry into ESG reporting based on the needs and maturity level of each company. Depending on the case, companies can choose to apply only the basic module or both modules, according to their CSR maturity and the expectations of their stakeholders.

The recommended core module

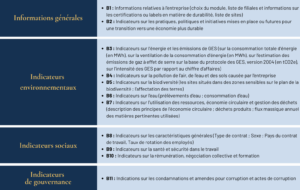

The first module, also called the “recommended core,” addresses 11 fundamental themes, from general company information to the main ESG indicators to be shared. This core constitutes a structuring and proportionate entry point for companies wishing to highlight their sustainability commitments without weighing down their organization. It is particularly suitable for micro-enterprises, for which it often provides a sufficient level of information. This basic module does not make double materiality analysis mandatory.

Furthermore, it gives companies the freedom not to respond to indicators that are not relevant according to the specificities of their activities. The calculation of greenhouse gas emissions is targeted at Scopes 1 and 2, representing the company’s direct emissions and those related to energy consumption. This approach allows for a more pragmatic measurement of the carbon footprint and facilitates the identification of concrete levers for environmental improvement.

The narrative module

The second module, known as the “narrative” module, enriches the basic module with a qualitative approach to sustainability strategy, a double materiality analysis, and advanced indicators regarding inclusion, climate, governance, and the economic model. This module highlights sustainable business models, the added value of diversity and inclusion, as well as climate risks and adaptation strategies.

It also explores greenhouse gas emission reduction policies, adopting a more narrative approach. This tool allows companies to structure and showcase their best practices while highlighting their concrete actions in favor of sustainability. By choosing this module, companies also formalize a strategic roadmap, structured around clear objectives and measurable results, while identifying the human, financial, or organizational resources necessary for the implementation of their sustainability reporting. It also requires a double materiality analysis of the sustainability issues specific to the company.

This module provides essential strategic data to business partners, investors, and lenders, meeting the growing requirements for sustainability information from their suppliers. These additional data points play a key role in evaluating the sustainability profile of the company that has adopted VSME reporting, whether as an established or potential supplier. By anticipating the requirements of these stakeholders, companies strengthen their strategic positioning and facilitate their integration into a committed ecosystem.

A framework aligned with European dynamics

The VSME follows the same logic of transparency as the European Sustainability Reporting Standards (ESRS) and the Corporate Sustainability Reporting Directive (CSRD), all supported by EFRAG. These standards aim to improve the comparability and reliability of sustainability information published by companies, whether they are large corporations or SMEs.

The CSRD, ESRS, and VSME provide a concrete response to the growing demand for transparency expressed by investors, clients, and financial and commercial partners. These actors now seek reliable, readable, and comparable ESG data to guide their decisions. Beyond compliance, these standards are fully in line with the ambition of the European Green Deal : to make the European Union a climate-neutral economy by 2050, by mobilizing the entire economic fabric toward a more responsible and resilient trajectory.

In this context, transparency regarding the ESG performance of companies becomes an essential lever for directing financial flows toward the most virtuous economic actors. Specifically, these standards cover the three ESG themes :

- Environment

- Social

- Governance

Particularly on topics such as climate change, resource management, diversity, human rights, and corporate governance, among others.

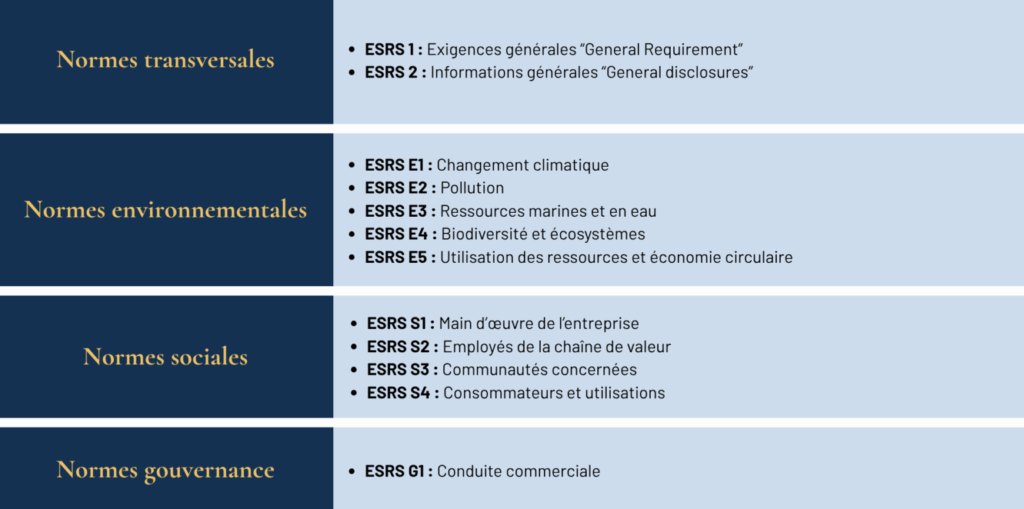

In this logic, the sustainability reports required by the CSRD are based on a common foundation: the 12 ESRS standards, which govern all information to be published, from the business model to ESG indicators. Designed according to a modular and proportionate logic, these standards adapt to the size and complexity of companies. They are mandatory for large companies and certain listed SMEs, while the VSME adopts these principles in a voluntary, simplified version that is perfectly accessible to non-listed SMEs wishing to structure their sustainability approach today.

Finally, these three sets of standards have a clear objective : to strengthen the transparency of extra-financial data. This level of clarity not only facilitates companies’ access to sustainable financing but also allows SMEs and mid-caps to better integrate into the value chains of large companies already subject to the CSRD, by responding in a structured and credible manner to their ESG requirements.

The CSRD, the ESRS, and the VSME therefore share a common philosophy : to structure, harmonize, and facilitate ESG reporting for all European companies, with requirement levels adapted to their size and status. The three mechanisms are part of the same transition dynamic toward a sustainable and transparent economy.

An opportunity to seize now

Designed for non-listed companies with fewer than 250 employees, the VSME offers a voluntary, flexible, and progressive framework, with no audit requirement. Much more than a simple communication exercise, it becomes a true strategic lever to showcase commitments, gain the trust of partners, and stand out in an environment increasingly attentive to ESG issues. Inspired by the structure of the CSRD, the VSME allows for the initiation of a sustainability approach at one’s own pace, with appropriate resources and without regulatory overload. It is the ideal way to lay the foundations for structured, effective, and accessible reporting.

Voluntary today, the VSME is a powerful lever for anticipating market expectations. It allows SMEs to capture financing that integrates ESG criteria, to gain competitiveness during tenders, and to structure a CSR policy in their own image. Finally, a structured framework for communicating sustainability information allows companies to manage their CSR strategy in a concrete way, while maintaining control over costs and priorities.

A choice that is all the more relevant as, by the end of 2025, with the transposition of the Omnibus I Directive, all companies with fewer than 1,000 employees could be affected by this voluntary standard. Adopting the VSME now means transforming a potential regulatory constraint into a strategic advantage.

How to deploy the VSME ? A step-by-step approach

To effectively integrate the VSME, we recommend a four-step approach:

- Assess the CSR maturity of the company and identify priority themes

- Collect data already available and detect any gaps

- Structure the information according to the chosen module, in a clear and readable manner

- Highlight the report through appropriate media and share it with stakeholders

An annual publication allows for showcasing efforts over time and anchoring sustainability in the corporate strategy.

Conclusion

In an environment where sustainability is becoming a decisive selection criterion, SMEs have everything to gain by anticipating new expectations. The VSME standard offers an accessible, readable, and recognized framework to structure your ESG approach without weighing down your organization. Flexible, voluntary, and aligned with the CSRD, the VSME is much more than a compliance tool: it is a true lever for transformation and value creation.

Ready to get started ? NG Audit supports French SMEs in the implementation of their VSME reporting, with a tailor-made method adapted to your challenges. Get a head start: make your commitment to sustainability a driver for growth. Contact us!